Traeger, Inc (COOK)

Heating up after 2Q Earnings Ignite a Breakout

Summary

Traeger is the category leader of innovative wood pellet grills, which have been taking market share from traditional gas and charcoal grills.

Through its digital content and marketing strategies, the brand has created a cult-like following that drives engagement and repeat purchases.

It has experienced two straight down years amidst supply chain problems and a soft consumer environment. This has left the company highly leveraged and pulling back from its growth strategy, focusing more on middle and lower funnel marketing spend and profitability.

With a typical replacement cycle of 5 years, the company is lapping its upgrade cycle from the lumpy 2020-2021 cohort in 2025, which may prove to be a significant year for its turnaround.

Interest rate cuts and a subsequent pick up in home sales should provide positive tailwinds and further catalyze the turnaround.

Company Description

Traeger is the creator and category leader of the wood pellet grill, with more than 50% market share in pellet grilling. The outdoor cooking system uses all-natural hardwoods to grill, smoke, bake, roast, braise, and barbecue. Its grills are versatile, easy to use, and technologically innovative. The ‘internet of things’ devices allow owners to program, monitor, and control their grill through the Traeger app. Data from its WiFi-enabled grills provide valuable insight to the company to better understand cooking habits, including which recipes are used, how long cook cycles last, the grill temperature, etc.

The company produces a significant amount of digital content across different channels, including instructional recipes and videos that are a powerful resource to its users. Its active online presence drives significant customer engagement and has created a sort of cult-style brand, which calls themselves the Traegerhood. Its marketing strategy focuses on empowering Traeger owners to deepen their cooking skills; and provides branded content highlighting stories, community members, and lifestyle content.

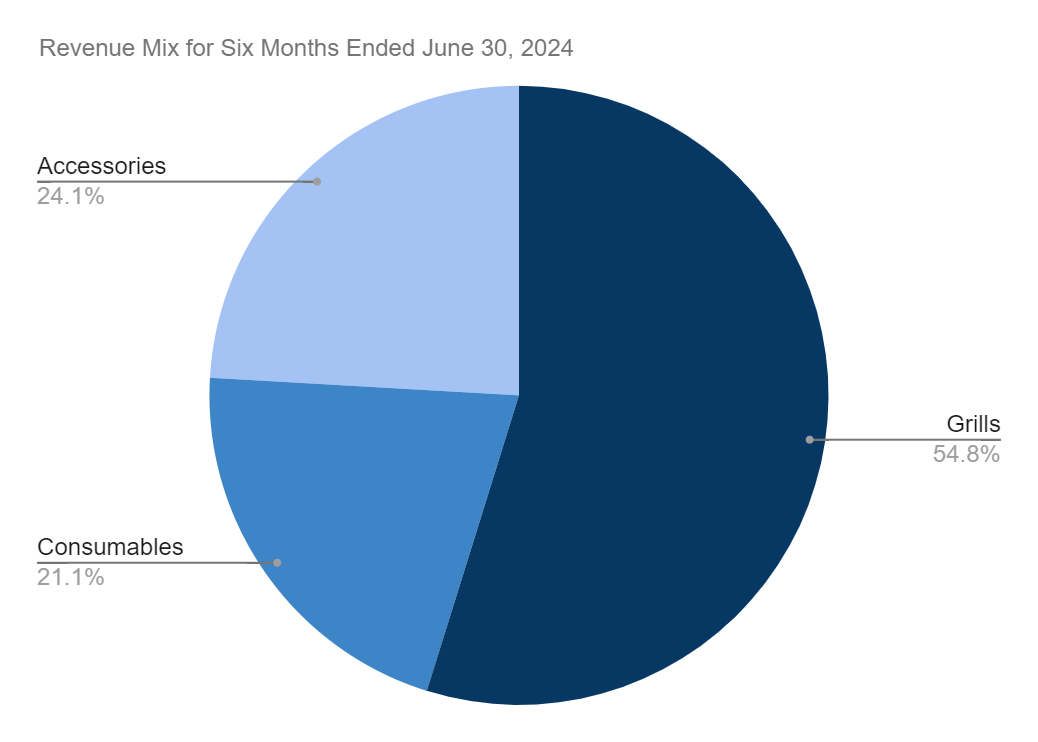

Operating Segments

Its pellet grills are the core of its platform and are complemented by Traeger wood pellets, rubs, sauces and accessories. Its three segments are shown below:

Source: Zuiderwind Research, COOK 10-K

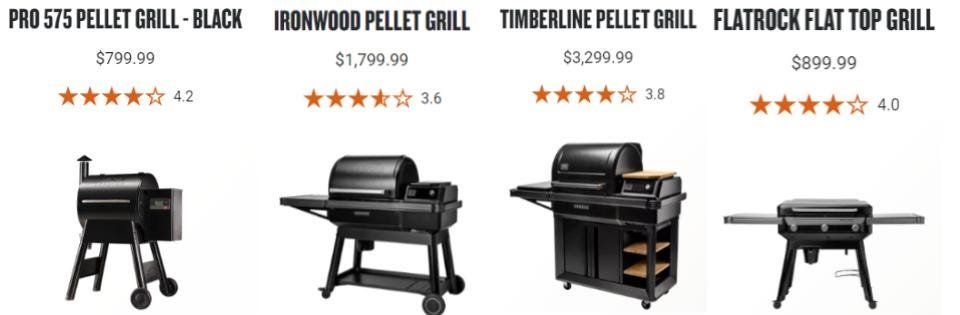

The grills segment currently has seven series of grills. The primary products are the Pro, Ironwood, Timberline, and Flatrock.

Source: Traeger.com

It offers portable grills at a lower price point in its Town and Travel Series, and additional models in targeted channels.

The consumables segment includes its wood pellets available in a variety of flavors, as well as rubs and sauces.

Its accessories segment includes recent acquisition MEATER smart thermometers, P.A.L. Pop-And-Lock accessory rails, grill covers, liners, tools, apparel and other ancillary items.

Market Environment

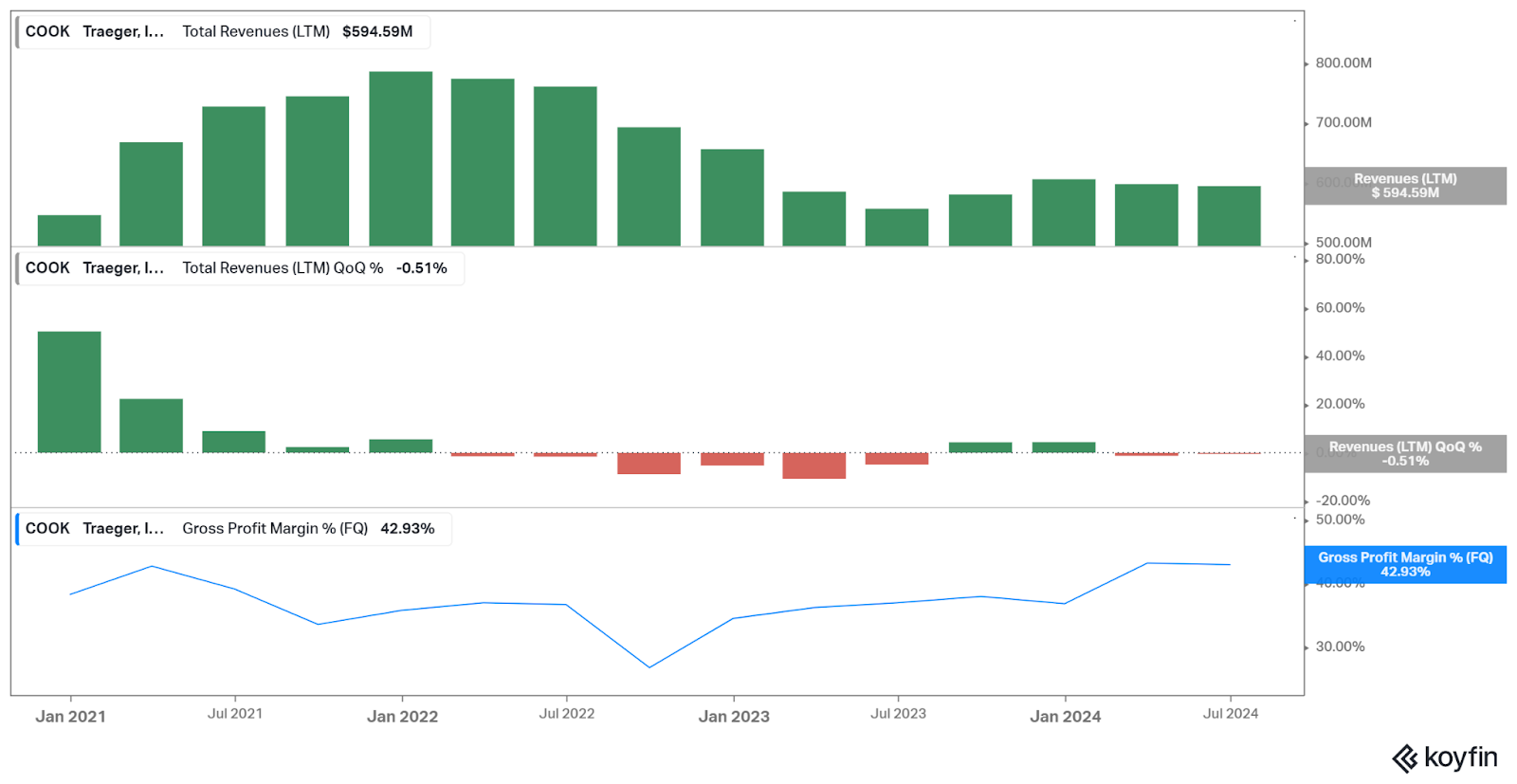

The company IPO’d in the summer of 2021, amidst the boom in consumer spending following the stimulus sent out by the US. With the stimulus checks around $1,200 per person and restaurants across the US forced to close, it created the perfect storm for Traeger. Sales were up 50% in 2020 and 44% in 2021, and compared to its historical top line growth rate around 20-30%.

Source: Koyfin

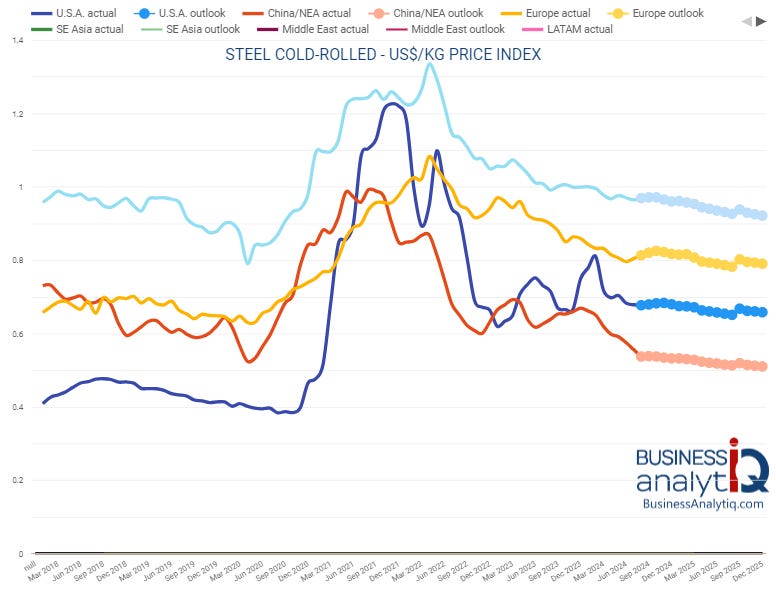

Similar to most other consumer goods companies at the time, the positive windfall for top line growth came with frustrations as supply chains broke down, causing gross profit margins at COOK to fall from over 40% to 26% in 2022, shown in the chart above. Its primary factories are located in China, so they saw significant headwinds with inbound transportation rates and changes in FX markets. Furthermore, one of its primary inputs, cold-rolled steel, saw significant volatility in price which pressured the cost of goods sold.

Source: BusinessAnalytiq

Just as supply chains and commodity markets began to normalize into 2023, the demand backdrop for consumer goods deteriorated.

Traeger’s management pivoted well from a focus of top-of-funnel marketing to its middle and lower funnel to reduce unnecessary marketing spend as consumers pulled back. It focused on general efficiency across its fixed cost structure, and has since gained significant ground on margins.

The category is now running on two straight years of negative growth, with hopes of the category bottoming in 2024. Traeger is looking to resume its expected long-term targets of revenue growth around 20% and 45% gross margin.

Inflection Point in the Replacement Cycle

As we round out 2024, it seems the market may be sniffing out an inflection point in the category and Traeger more specifically. The typical product replacement cycle for a Traeger grill is 5 years vs an industry average of 7-8 years. This shorter replacement cycle is driven by its innovation and technology cycles, as consumers look to upgrade to keep up with new software and new capabilities. Additionally, Traeger grills tend to get more use than a traditional grill, and are used year round instead of just in the summer.

2025 may prove to be a significant moment in the replacement/upgrade cycle, as we will lap the lumpy 2020-2021 cohort of first time purchasers. The risk is that this cohort is less likely to be a repeat buyer since their grill was essentially paid for by the U.S government. Given that Traeger has solid insight into customer engagement through the use of its app and web content, I expect that the guidance they’re giving accounts for any differences within the cohorts differing use and spending habits.

Correlation to Interest Rates and Home Sales

In its most recent earnings call, the CEO, Jeremy Andrus, gave an insightful comment on the impact of interest rates on its business.

There are absolutely direct -- direct sort of correlations between interest rates and Grill demand… $1,000 purchase often is financed either on our website through a financing partner, at retail through financing programs that they offer.

There is also a correlation between housing transactions and new grill purchases. And while that doesn't drive most of our business, it certainly influences 15% to 20% of the business. And given where interest rates have been, housing transactions are very low… We begin a new cycle where interest rates come down, the consumer gets healthy.

When interest rates are high and [the] consumer is relatively weak, purchases are pushed out unless they're absolutely necessary. And so we expect to benefit from that. And I think the combination of a healthier consumer, but also investments that we've been making in product and increased investments in brand and top of funnel that we plan, we believe that we'll take share. And I think the combination of the 2 will be meaningful for our business.

Source: Koyfin, COOK 2Q2024 Earnings

Lower interest rates could be a significant tailwind as financing costs come down, home transactions pick up, and the consumer begins to loosen up on spending.

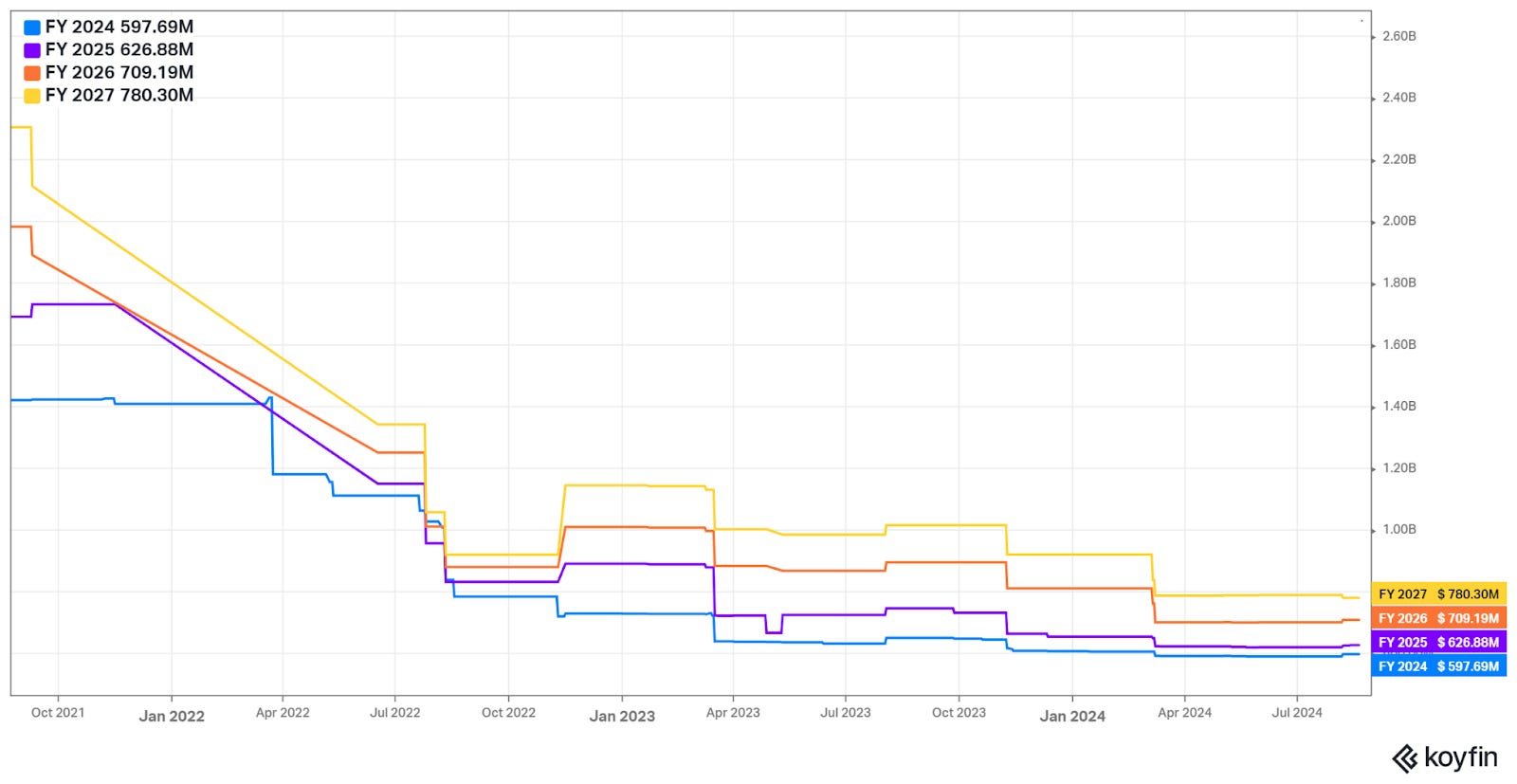

Rock Bottom Expectations

Analysts have spent the last 3 years revising down estimates (which in hindsight were overly optimistic) from a range of $1-2 billion in revenue for FY 24’ - 27’ to just $780 million for FY 2027. These low expectations provide for meaningful upside surprises as the consumer environment strengthens and the company continues to execute on its growth strategy after years of tightening the belt for the sake of profitability.

Source: Koyfin

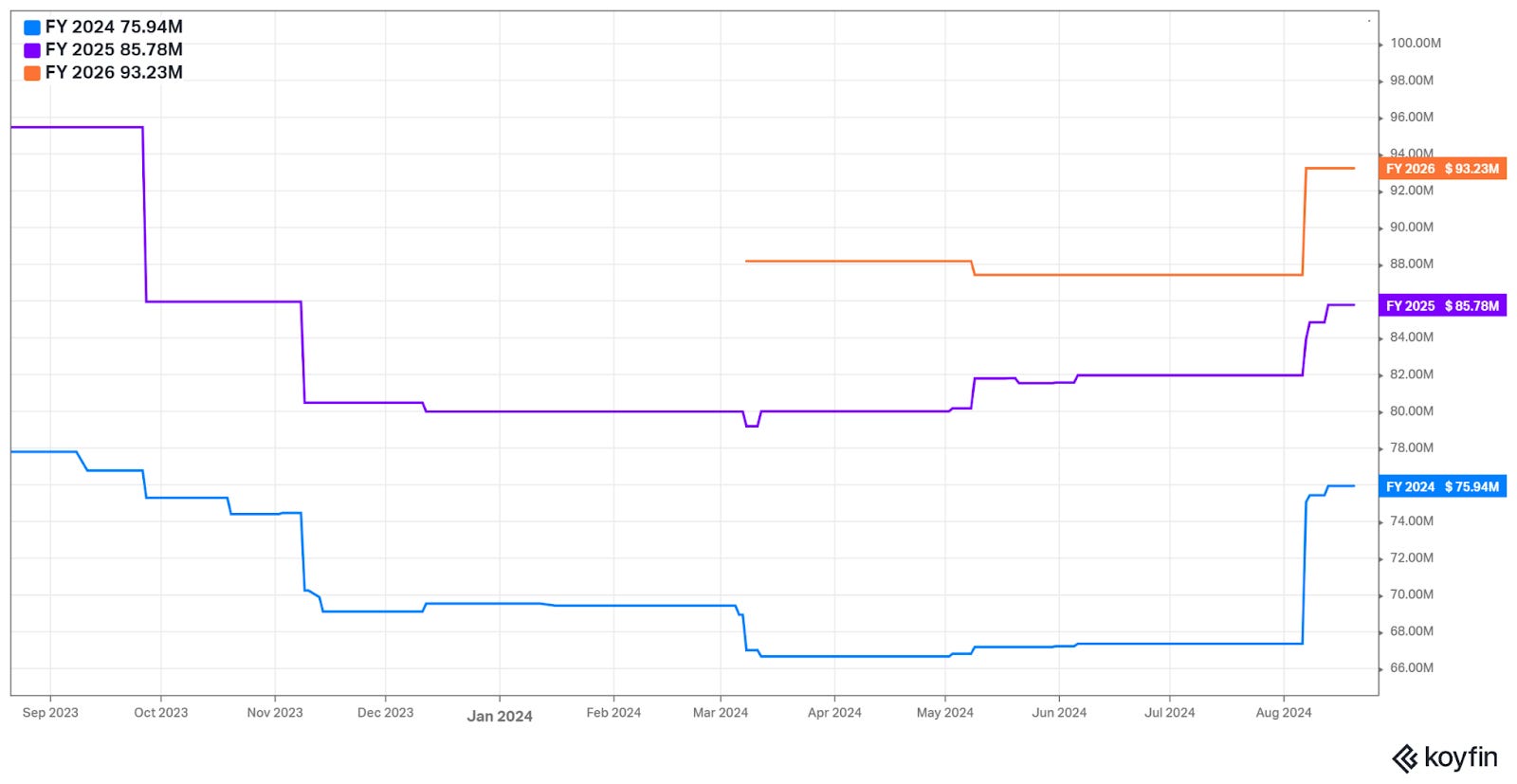

In its recent quarter, it had gross margins of 42.9% vs the Street’s estimate of 39.7%, up 600 basis points compared to the prior year. This resulted in adjusted EBITDA of $27 million, a 25% improvement from the second quarter last year. The better-than-expected results gave the market further confidence that a turnaround is underway, with shares up 24% on the news. Analysts raised EBITDA estimates up meaningfully across models, underscoring the negative sentiment that has previously been present in the stock and potentially beginning a new trend of upward revisions.

Source: Koyfin

Valuation

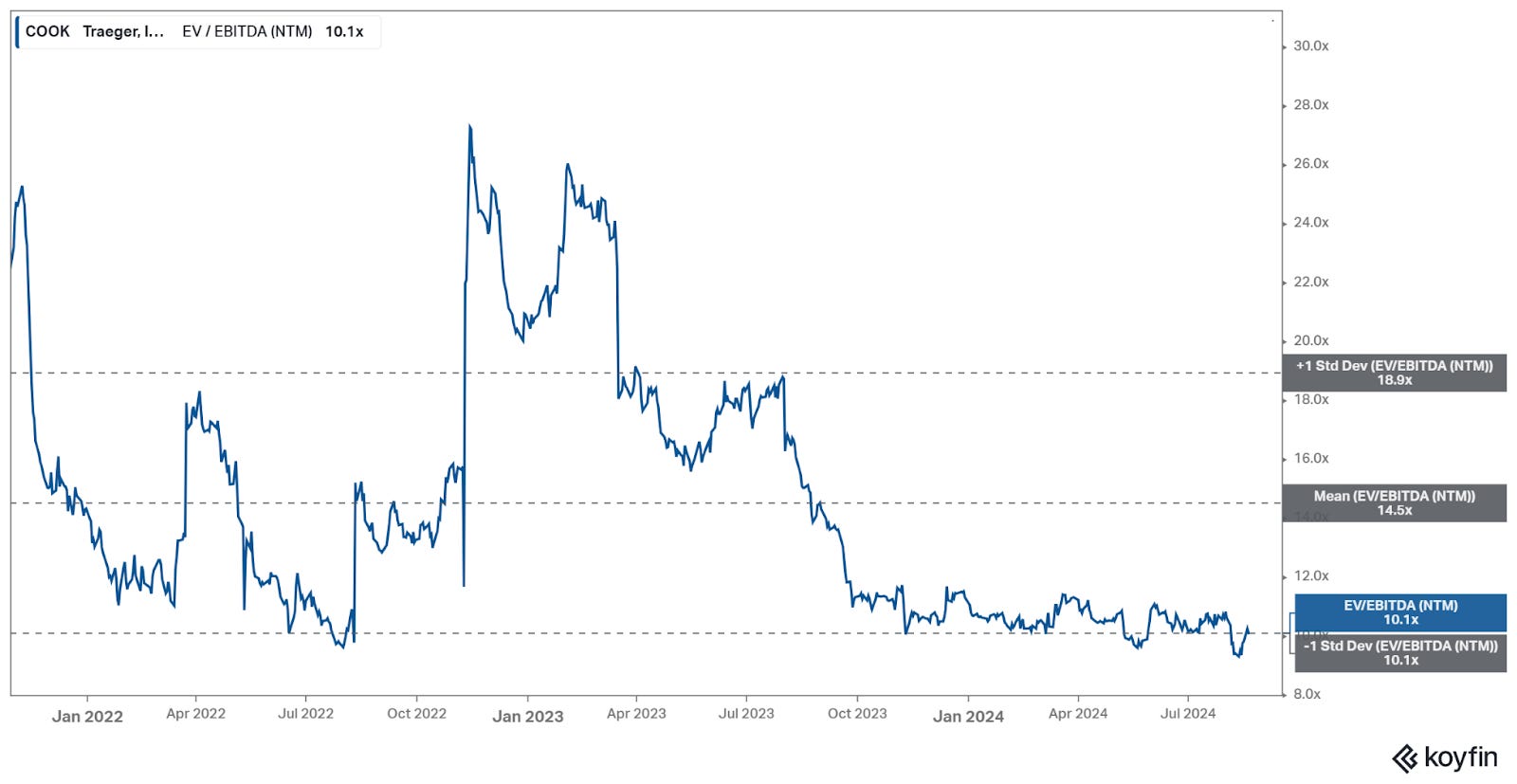

EV/EBITDA (NTM) is around 10x currently, which has been the bottom of its range over the last several years. As the category stabilizes, and given its longer term growth prospects and strong brand recognition, I expect it to trade closer to 12x-14x.

Source: Koyfin

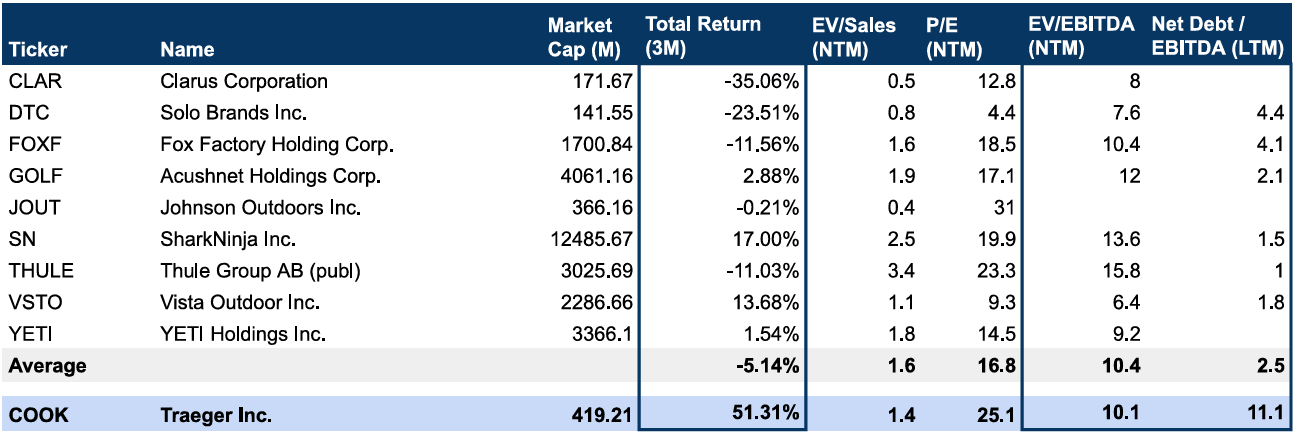

Comps

Source: Zuiderwind Research, Koyfin

In terms of momentum, Traeger has diverged significantly, up over 50% in the last 3 months versus a peer average of -5%.

On a relative and absolute basis, the company is extremely leveraged, with net debt/EBITDA around 11x, and a debt/equity ratio of 1.5x. Positive EBITDA growth of late has contributed to some deleveraging, but there still is significant risk to the balance sheet if the operating environment worsens.

Breakout on Strong Volume

The recent breakout of the 100-day high after the earnings pop on August 6th has sustained nicely with outsized volume, holding well above the $3 level that it has been trapped in for the last year. My signal was the breakout above this level, with a stop around 20-25% from entry. Given the heightened volatility lately, this wider stop should leave enough room to not get shaken out on a pullback.

Source: TradingView

As always, nothing I say is investment advice, please seek advice from an investment professional on your unique situation. The writing is for informational and educational purposes only, and is not an offer to buy or sell securities mentioned. I may hold positions long or short in securities mentioned, and positions are often a small percentage of my overall portfolio. I will not be writing in a regular, predictable basis, please do your own due diligence on any topics mentioned.